Domo, Inc. — Sell-Side M&A Pitch Case Study

Case Completion Date: 04/10/2026

Case Upload Date: 05/12/2026

This case study was built as a full sell-side M&A pitch for Domo, Inc. (NASDAQ: DOMO), a cloud-native business intelligence and AI data platform. The work product includes a complete three-statement financial model with DCF, public comparable company and precedent transaction analyses, a buyer universe, and a formal pitch deck.

The thesis was contrarian by design. In early 2026, a broad SaaS de-rating driven by rising rate persistence, slowing enterprise IT budgets, and multiple compression across the software sector left fundamentally improving businesses trading near distressed levels. Domo was one of them. Despite six consecutive quarters of NRR improvement, a deepening integration with major cloud data warehouses including Snowflake, and a shift toward high-retention consumption-based pricing, the market was pricing the company as though the turnaround had not happened.

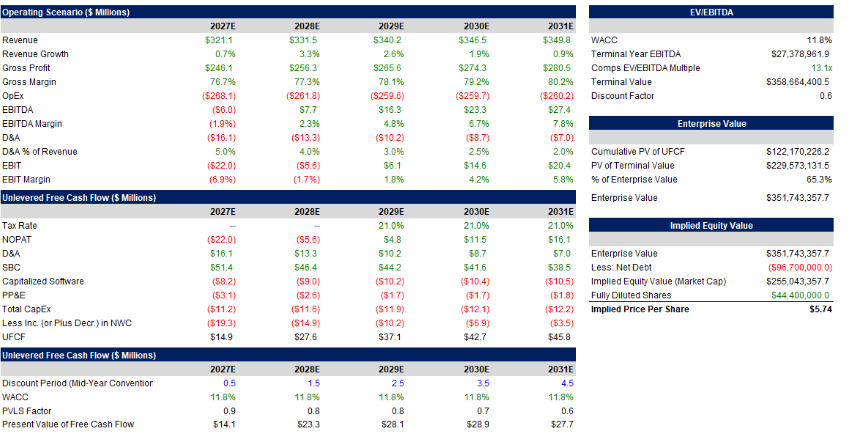

My analysis identified Domo as substantially undervalued with a blended price target of $4.93, weighting public comps, a DCF, and precedent transactions. At case completion, Domo traded at $2.67. The stock has since climbed over 40% to $3.80, and my target still represents more than 30% additional upside from today. The gains have not changed my conviction, only affirmed it, though I could not have anticipated a correction of this magnitude in such a short period of time.